Titan Capital Recovery Group is an advisory firm with over twenty-five years of experience that structures transactions and relationships to holistically develop solutions for clients and/or their advisors, considering the client’s specific situation, with a focus on liquidity, exit opportunities, corporate or personal income taxes by integrating tax strategies that minimize, defer, recapture or eliminate taxes that conform to rules-based constraints in law, accounting, regulation, tax, etc..

The Power Hedge is an investment in a solar power generation facility. This investment combines above average yield opportunity combined with significant tax incentives which include a 26% investment tax credit (ITC) and significant accelerated depreciation. Qualifying investors may be able to utilize the ITC and accelerated depreciation during the year 1. The tax incentives include a 26% (for projects which are brought online in 2020, and approximately 87% of the project investment. These benefits may be rolled forward 20 years, as well as being used against the previous tax year. Assuming the current tax year has been filed, the tax payer is able to amend past 3 years of returns. Yield income is backed by twenty plus years of power purchase agreements with high credit quality entities. This income has limited volatility nor is the payment correlated to the overall performance of the equity or debt markets. After six years of operation, the investor may choose to sell, or hold their Solar Development.

The Research and Development (R&D) Tax Credit remains one of the best opportunities for businesses to substantially reduce their tax liability. For what amounts to their daily activities, companies from a wide-range of industries can qualify for federal and state tax savings high to enough to allow companies to hire new employees, invest in new products and service lines, and grow their operations.

Now, due to numerous modifications and expansions over the years, more companies than ever before can benefit from this valuable incentive.

However, what constitutes R&D with regard to the credit is much more expansive than business owners realize, with activities related to applied sciences and other technical projects qualifying companies from numerous industries.

The R&D Tax Credit is for businesses of all sizes, not just major corporations with research labs – and many companies are eligible, with an expansive list of activities qualifying for the credit.

Benefits

Cost Segregation is a commonly used strategic tax planning tool that allows companies and individuals who have constructed, purchased, expanded or remodeled any kind of real estate to increase cash flow by accelerating depreciation deductions and deferring federal and state income taxes.

A cost segregation study identifies and reclassifies personal property assets to shorten the depreciation time for taxation purposes, which reduces current income tax obligations. Personal property assets include a building’s non-structural elements, exterior land improvements and indirect construction costs. The primary goal of a cost segregation study is to identify all construction-related costs that can be depreciated over a shorter tax life (typically 5, 7 and 15 years) than the building (39 years for non-residential real property). Personal property assets found in a cost segregation study generally include items that are affixed to the building but do not relate to the overall operation and maintenance of the building.

A Cost Segregation study allows a taxpayer who owns real estate to reclassify certain assets as Section 1245 property with shorter useful lives for depreciation purposes, rather than the useful life for Section 1250 property.

Recent tax law changes under the Tax Cuts and Job Act of 2017 (TCJA) have given a boost to cost segregation. Bonus depreciation was increased from 50% to 100% on certain qualifying assets. Real estate investors will receive immediate expensing of certain 5, 7 and 15 year property. TCJA also allows used property that was acquired after Sept. 27, 2017 to qualify for this special depreciation treatment. A quality cost segregation will separate any costs that qualify under the new bonus depreciation rules.

Unique tax deferral strategy for “HIGHLY APPRECIATED ASSETS” with low basis. The strategy allows the seller to sell the asset and defer 100% of the capital gains taxes up to 30 years. Additionally, Installment Sales are useful for lowering capital gains taxes, where the income can be delayed until they are taxed at lower rates.

However, there are two requirements for an installment sale. The first is that if an asset is sold and payments will be made over time that at least one payment be received a year after the tax year of the sale. The second is that the installment sale is recorded on Form 6252.

Benefits

Ecosystems, species, wild populations, local varieties and breeds of domesticated plants and animals are shrinking, deteriorating or vanishing. The essential, interconnected web of life on Earth is getting smaller and increasingly frayed,” “This loss is a direct result of human activity and constitutes a direct threat to human well-being in all regions of the world.”

America is losing two football fields of land every minute to development, putting species at risk and permanently changing our nation’s wildlife. Conservation partnerships help protect these precious lands and species from development in perpetuity.

Land conservation has never been more important, and the significant conservation achieved through partnerships enables more Americans to participate and protect more lands with both high conservation values and high development potential.

IRS rules would allow the taxpayer to deduct up to 50 percent of their income for the year in which the easement agreement was created and continue deducting up to 50 percent of their income for 15 additional years or until the full deduction is claimed, whichever comes first.

Benefits

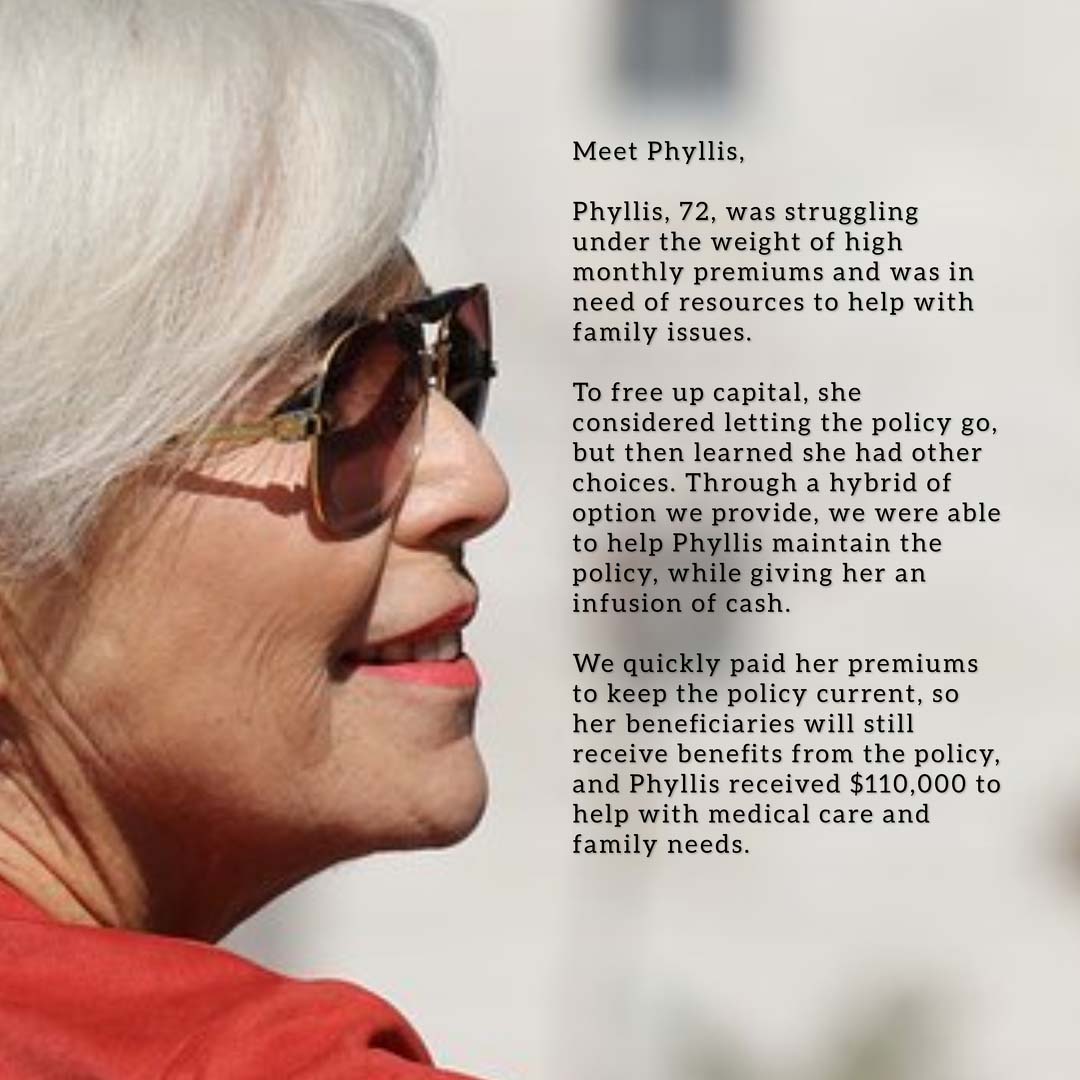

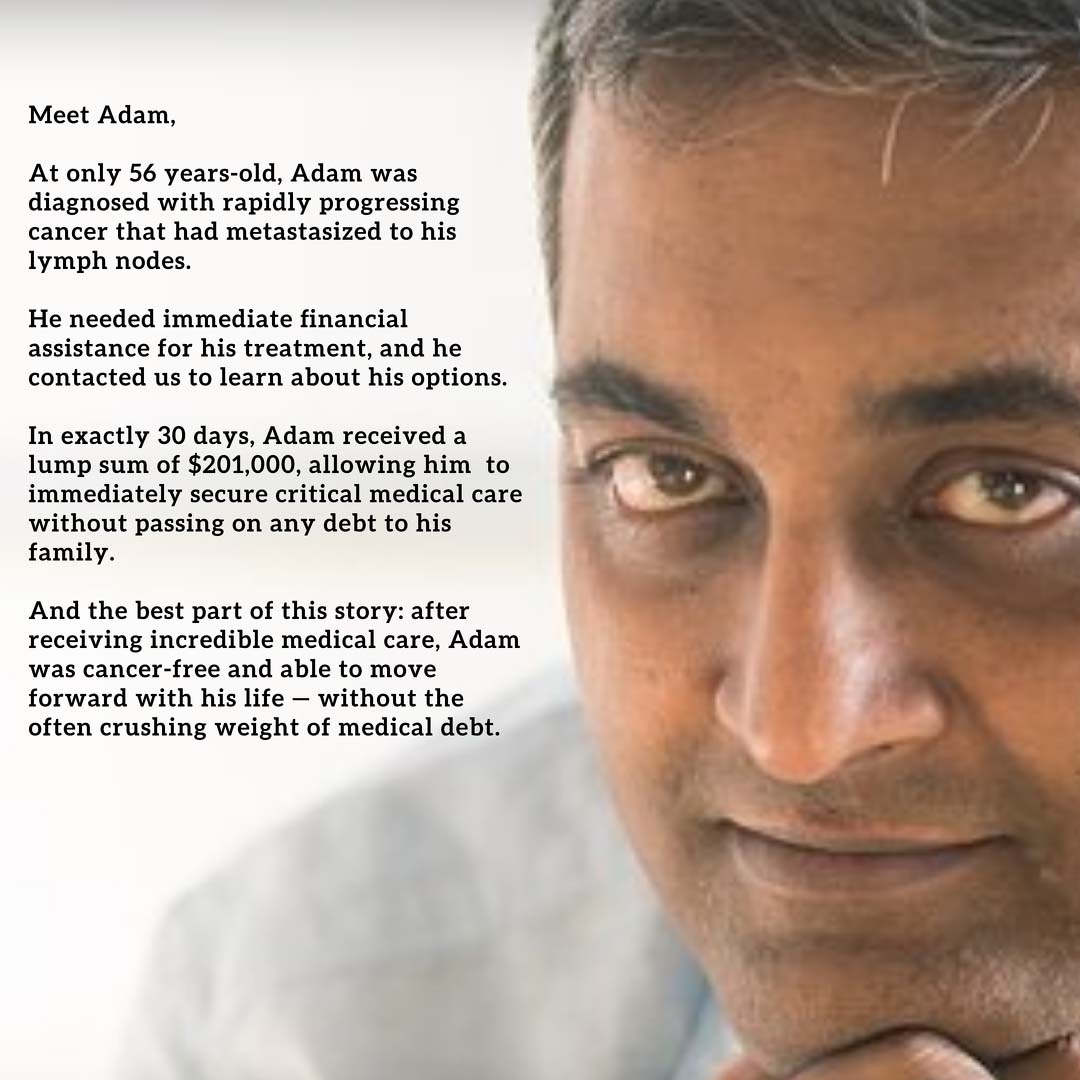

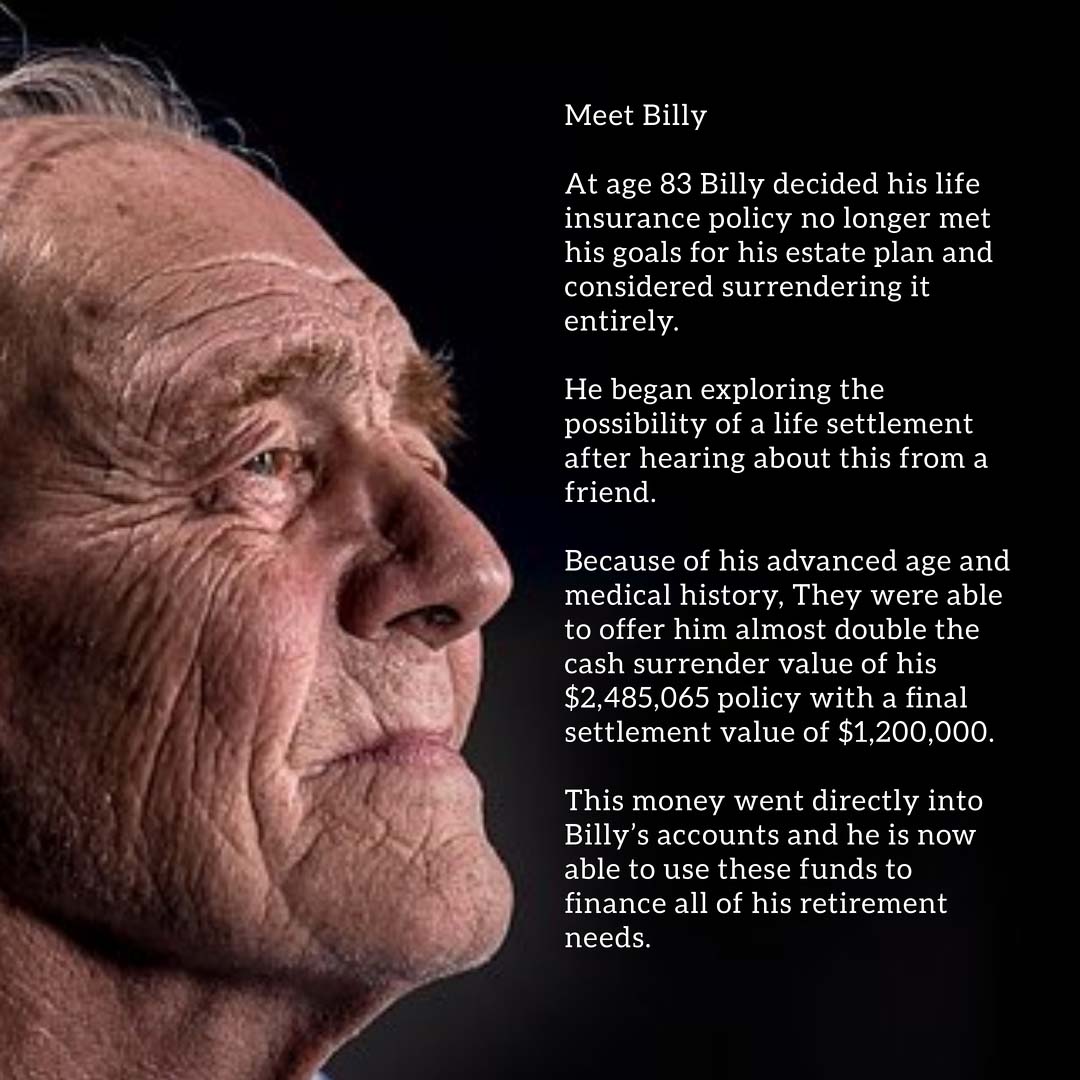

Life insurance is often a senior’s largest asset and one they can use to alleviate retirement challenges – but they do not treat it that way. They rarely realize it belongs to them, not the insurance company, and can be sold if they believe there is a better use for the equity they have built.

At Hotaling Insurance Services (H.I.S.), we want to provide the information your client deserves, so they can decide if selling a policy, or a portion of it, is right for them.

How It Works

1. Policy owner completes a simple intake form.

2. H.I.S. will collect in-force illustrations and up-to-date medical records on the insured(s).

3. The medical records are sent to third-party underwriters to determine longevity.

4. H.I.S. offers a fair market value through Net Present Value calculation using longevity and cost of insurance.

5. Clients sign final contracting documentation and receive funding post ownership change.

Ideal Candidates

• Insureds over the age of 75

• Clients with an immediate need for liquidity

• Life insurance policies that have been underfunded or underperformed

• Policies on the verge of lapsing

• Premium financed policies

• Trust owned life insurance policies

Benefits

• Increase Client Liquidity

• Remove Premium Exposure

• Reappropriate Funds to Different Products

• 8x Cash Surrender Value

The production companies may sell or otherwise transfer the credit, but the transferee may only use it in an income year when the production company could have used it. The credit may not be refundable. Companies may sell or otherwise transfer their credits, but the law may limit them to three transfers.

Movie production incentives are tax benefits offered on a state-by-state basis throughout the United States to encourage in-state film production. These incentives came about in the 1990s in response to the flight of movie productions to other countries such as Canada. Since then, states have offered increasingly competitive incentives to lure productions away from other states. The structure, type, and size of the incentives vary from state to state. Many include tax credits and exemptions, and other incentive packages include cash grants, fee-free locations, or other perks. Proponents of these programs point to increased economic activity and job creation as justification for the credits.

Production companies must often meet minimum spending requirements to be eligible for the credit. Of the 28 states that offer tax credits, 26 make them either transferable or refundable. Transferable credits allow production companies that generate tax credits greater than their tax liability to sell those credits to other taxpayers, who then use them to reduce or eliminate their own tax liability

Benefits: